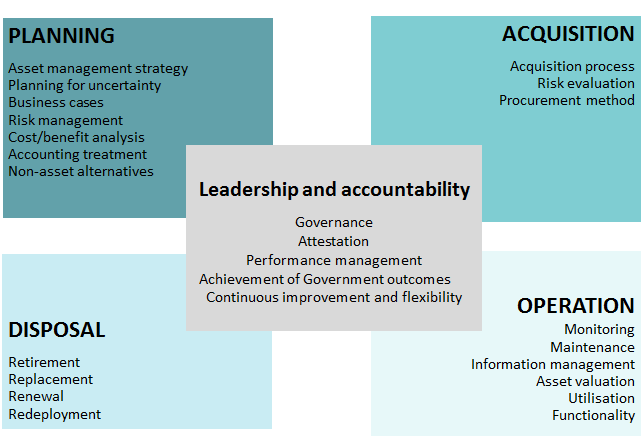

The four key stages of the asset lifecycle are:

- Planning: determination of asset requirements, based on an assessment of both service delivery needs and the capability of the existing asset base to meet these needs.

- Acquisition: procurement of assets to meet an identified service need, including the assessment of procurement options.

- Operation and maintenance: management and use of an asset to deliver services, including maintenance.

- Disposal: treatment of an asset that has either reached the end of its useful life, is considered surplus, or is under-performing.

These stages are represented in the diagram below as occurring sequentially, but each stage will be informed by activities occurring in each of the other sectors:

Organisational leaders are expected to promote principles and policies for good asset management throughout all stages of the asset lifecycle.

Asset Management Accountability Framework

The Asset Management Accountability Framework (AMAF) replaces Victoria’s existing asset management framework, Sustaining Our Assets and the related asset management series. The AMAF assists Victorian Public Sector agencies manage their asset portfolios and provide better services for Victorians.

Like Sustaining Our Assets, the AMAF is premised on a non-prescriptive, devolved accountability model of asset management. This allows public sector bodies to manage their assets in a manner that is consistent with government requirements, their own specific operational circumstances and the nature of their asset base.

The AMAF details mandatory asset management requirements as well as general guidance for agencies responsible for managing assets. Mandatory requirements include developing asset management strategies, governance frameworks, performance standards and processes to regularly monitor and improve asset management. The requirements also include establishing systems for maintaining assets and processes for identifying and addressing performance failures.

Additionally, secretaries and public sector boards, must attest to their agency’s compliance with the mandatory requirements of the AMAF in their annual report from 2017-18 and, every three years, self-assess their organisation's asset management maturity.

The AMAF applies to non-current assets (physical and intangible) but not financial assets, controlled by government departments, agencies, corporations, authorities, and other bodies that are captured by the Standing Directions of the Minister for Finance made under the Financial Management Act 1994 (FMA).

Implementation guidance

Implementation guidance has been developed to assist public sector agencies implement the AMAF.

The guidance is not compulsory. It offers potential approaches, and summarises some of the possible inputs and evidence, that could be used to document compliance with the AMAF mandatory requirements. The guidance has been drafted to be of greatest assistance to those uncertain of where to begin.

This guidance incorporates and supersedes previous AMAF guidance material released with the framework in February 2016 and updated in June 2016.

Asset management maturity assessments

To support the dual goals of increasing transparency and working towards best practice in asset management, departments and agencies will need to complete a self-assessment of their asset management maturity and present this in their 2020-21 annual reports, with further assessments every three years.

Completing a maturity assessment allows government entities to compare their actual performance with their desired performance and better understand ‘what to improve’ to optimise cost, risk and asset performance.

In February 2021, DTF published guidance for the self-assessment of asset management maturity. Departments and agencies should tailor their approaches to compliance depending on the size, complexity and risks associated with their asset holdings.

The guidance includes a rating system to be used by all departments and agencies in undertaking maturity self-assessments, unless an alternative assessment tool has been discussed with DTF in advance of the commencement of the 2020-21 self-assessment reporting.

DTF has also published a compliance tool allowing entities to:

- establish a target maturity level for the AMAF requirements (which may change over time)

- assess the system status and effectiveness of application for the AMAF requirements

- present evidence to substantiate an assessment

- consider whether a compliance deficiency is material

- outline remedial actions and a timeframe, where applicable.

The compliance tool allows entities to develop an overall assessment of their asset management maturity which can be readily presented in an annual report.

Maturity assessments should also be peer-reviewed to ensure assessments are appropriate and evidence-based.

Ideally, maturity assessments should be informed with input from key business functions covering engineering/maintenance, procurement, information, financial, operations and human resources.

Below is the Guidance Note: Adopting a risk-based approach to AMAF compliance assurance and maturity assessment and the compliance tool that can be used by departments or agencies to assess their maturity against AMAF requirements.

Updated